Guaranty associations are state-sanctioned, nonprofit organizations that insure consumers in the unlikely event that their insurance companies fail and default on their payments. Insurance companies, which issue annuities, are legally required to belong to their particular state’s guaranty association.

By Elaine Silvestrini

The safety of investments is paramount to consumers. When Americans entrust their savings to money in federally regulated banks, their deposits are insured by the Federal Deposit Insurance Corporation.

That’s not the case with annuities, which are legally considered insurance products issued by insurance companies rather than banks. But that doesn’t mean customers are without protection. Instead of federal protection, individual states provide the protection similar to the FDIC.

That’s because insurance companies are regulated on the state level. State regulators monitor insurance companies’ finances and impose financial standards. They require corrective action when the companies’ fail to meet the standards, and they collect money from companies’ when needed to cover customer losses.

Each state, as well as the District of Columbia and Puerto Rico, has a guaranty association, and every insurance company must belong to the guaranty association in the state where they operate.

How Do Guaranty Associations Work?

Guaranty associations are funded by assessments levied against member insurance companies that help pay claims when a member company fails. The funds are combined with the failed company’s assets to pay claims up to statutory limits.

However, the coverage may not be necessary because often when an insurance company becomes insolvent, the company’s contracts are purchased by other insurance companies. So customers still have the same insurance and annuity contracts worth the same amount of money, only from different companies.

In addition to annuities, these associations cover life insurance policies, long-term care policies and disability income insurance policies. Most states have a cap of $300,000 in total benefits for any individual customer with one or more policies with the failed insurance company, according to the American Council of Life insurers.

To ensure you receive all your annuity benefits, it’s a good idea to investigate the ratings of the issuing insurance company before making an annuity purchase. If you plan on purchasing annuities worth more than your state guaranty association limits, you may want to purchase multiple annuities from different companies, without exceeding the guaranty limits on a single annuity.

Limits on Coverage

Guaranty associations are funded by assessments levied against member insurance companies that help pay claims when a member company fails. The funds are combined with the failed company’s assets to pay claims up to statutory limits.

However, the coverage may not be necessary because often when an insurance company becomes insolvent, the company’s contracts are purchased by other insurance companies. So customers still have the same insurance and annuity contracts worth the same amount of money, only from different companies.

In addition to annuities, these associations cover life insurance policies, long-term care policies and disability income insurance policies. Most states have a cap of $300,000 in total benefits for any individual customer with one or more policies with the failed insurance company, according to the American Council of Life insurers.

To ensure you receive all your annuity benefits, it’s a good idea to investigate the ratings of the issuing insurance company before making an annuity purchase. If you plan on purchasing annuities worth more than your state guaranty association limits, you may want to purchase multiple annuities from different companies, without exceeding the guaranty limits on a single annuity.

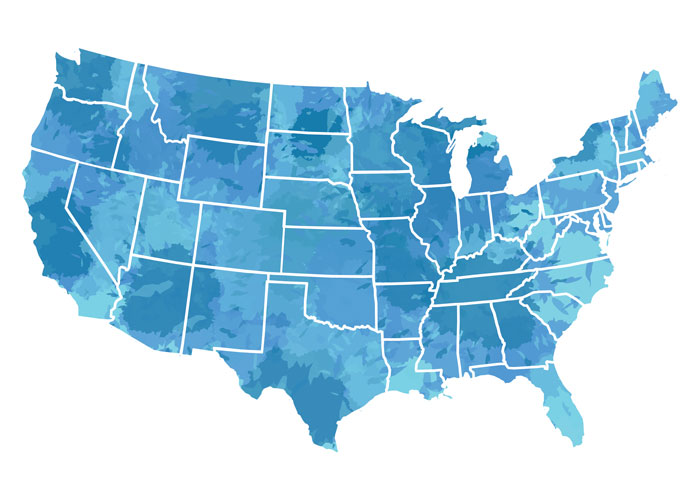

Annuity Protection by State

| Policyholder Protection: Annuity Benefit Limits | |

|---|---|

| $250,000 | |

| $250,000 | |

| $250,000 | |

| $300,000 | |

| 80% of the annuity contract value up to a $250,000 limit | |

| $500,000 | |

| $250,000 | |

| $300,000 | |

| $250,000 (if the annuity is deferred) or $300,000 (if the annuity is in payout status) | |

| $250,000 (if the annuity is deferred) or $300,000 (if the annuity is in payout status) | |

| $250,000 | |

| $250,000 | |

| $250,000 | |

| $250,000 | |

| $250,000 | |

| $250,000 | |

| $250,000 | |

| $250,000 | |

| $250,000 | |

| $250,000 | |

| $250,000 | |

| $250,000 | |

| $250,000 in most cases, or up to $410,000 for structured settlements and for annuities that have been annuitized for not less than lifetime or for a period certain not less than 10 years | |

| $250,000 | |

| $250,000 | |

| $250,000 | |

| $250,000 | |

| $250,000 | |

| $250,000 | |

| $100,000 (if the annuity is deferred) or $500,000 (if the annuity is in payout status) | |

| $250,000 | |

| $500,000 | |

| $300,000 for most annuities with an exception of $1,000,000 for structured settlement annuities | |

| $250,000 | |

| $250,000 | |

| $250,000 | |

| $300,000 | |

| $250,000 | |

| $250,000 | |

| $300,000 | |

| $250,000 | |

| $250,000 | |

| $250,000 | |

| $250,000 | |

| $250,000 | |

| $250,000 | |

| $500,000 | |

| $250,000 | |

| $300,000 | |

| $250,000 |

Got a question or comment? You can reach us at www.FreedomWealthServices.com or call us at 904-373-8349

To view more articles from Freedom Wealth Services visit: https://freedomwealthservices.com/news/