Business

October 2 2010

By MARK MAREMONT And LESLIE SCISM

(See Correction & Amplification below .)

The life-insurance industry has enjoyed beneficial tax treatment for its products for nearly a century. Whenever Congress tried to change that, insurers always had a mantra at the ready: We protect widows and orphans.

Life insurance needs to be free from income taxes, the industry said, because of its special social function. It keeps survivors from a life of penury when a chief breadwinner dies.

It’s common knowledge that the top 10% income earners have

access to the very sharpest CPAs, MBAs, Attorneys and

Financial Experts that money can buy. The logical conclusion is

that this retirement vehicle obviously meets and exceeds their

high standards of safety and security while producing above

average returns.

So the question is… What do they know that you don’t and why hasn’t your CPA or advisor told you about this?

The answer is at the end of this article…

Audio

How policies help the wealthy minimize estate taxes, Mark Maremont reportsBut in a development all but unnoticed outside the industry, life-insurance companies gradually have shifted away from their broad historical base of middle-class households. Instead, statistics show, an increasing portion of insurers’ business consists of selling large policies to wealthier Americans, often as part of complex estate-tax plans.

The shift means that a growing proportion of the tax benefits of life insurance goes to the well-off, not to the middle class that once was the industry’s backbone.

The industry’s safety-net role is eroding just as Congress is scouting for new revenue sources amid gaping budget deficits, raising concern among insurance executives that lawmakers could revisit the industry’s tax advantages.

There is no proposal in Congress this year to curb the tax breaks for life insurance. Washington insiders say any such attempt would likely face heavy opposition from insurers and agents, as well as from the general resistance to any kind of tax increase at a time when the economy is weak.

Still, “the vast majority of business in America is worried about the budget shortfall and the need for the federal government to ramp up revenue,” said Matthew Winter, president of Allstate Corp.’s Allstate Financial unit. For life insurers, “certainly it is a legitimate concern.”

AIG Chairman Discusses Troubled Insurer’s Future

10:54

In a milestone agreement, the U.S. Treasury will convert its ownership stake in insurance giant AIG to common shares. The gradual sale of those shares will help AIG repay the government’s $120 billion of support that kept AIG afloat in late 2008. AIG Chairman Robert “Steve” Miller discusses the agreement and AIG’s future with Neal Lipschutz, managing editor of Dow Jones Newswires.

The industry’s years-long shift toward wealthier buyers is clearest in “permanent” life-insurance policies, including varieties known as “whole life” and as “universal life,” which combine a death benefit with a savings or investment account. These represent almost three-fourths of individual-policy premiums collected.

They have a dual tax advantage: The death benefit isn’t subject to federal income tax, and earnings in the investment-account part generally accrue tax-free.

High-end policies for $2 million and up, which can carry annual premiums of $20,000 or more, made up nearly 40% of the face value of new whole-life and universal-life policies sold in 2007, according to an analysis done for The Wall Street Journal by Limra, an industry-funded research group. Such large policies accounted for just 10% a decade earlier, and 1% two decades ago.

Meanwhile, the percentage of American families owning life insurance continues to fall. Thirty percent have no life-insurance coverage of any kind, a four-decade high, according to a Limra survey.

Permanent life insurance has “become a tax shelter for the rich,” said Charlie Smith, a former head of an international association of insurance managers, who in 2003 to 2005 was chairman of an insurance-industry task force on flagging middle-market sales. “If the industry no longer has a significant presence on Main Street, it loses its political clout in Congress and can’t defend the tax benefits.”

Trevor Clark for The Wall Street Journal

Maryanne Ingemanson, 77, at her home on the shores of Lake Tahoe, Nev., uses a life-insurance policy as part of an estate-planning tax strategy.

Whole and universal life’s tax benefit could become still more important to affluent families if their income-tax rates rise, as they would under Obama administration plans to restrict the extension of the Bush-era tax cuts.

Meanwhile, middle-class families have been getting a smaller portion of the overall tax benefits, in part because they tend to hold less-costly “term” insurance, which provides coverage just for a designated period and doesn’t involve a tax-advantaged investment account.

With term insurance, the only tax break is an untaxed death benefit, and this break comes into play infrequently. That’s because most buyers are in their 30s or 40s and remain alive at the end of the policy’s term.

Some life-insurance executives say the tax advantages remain important because they encourage people of all income levels to buy protection against an eventuality many would rather not think about.

Frank Keating, president of the American Council of Life Insurers, said the favorable tax treatment of assets accumulated within insurance policies is justified even if the affluent are big beneficiaries, because “it is good public policy” to encourage wealth accumulation that helps feed capital formation and job creation.

Trade groups note that life insurers are long-term investors and among the biggest holders of the nation’s corporate debt, giving Congress a strong incentive to keep the tax advantages in place and avoid destabilizing a key player in the economy.

Mr. Keating also noted the crucial role that life insurance can play in helping small businesses survive the death of a founder.

“Declaring war on people who are savers and investors is not a positive agenda,” said Mr. Keating, a former Oklahoma governor. “That’s not to say we shouldn’t have the debate. We’ve had it, and we will always have it.”

Of the two main life-insurance tax preferences, the one that has faced the most scrutiny from Congress over the years is the provision that lets investment gains accumulate tax free within permanent-life policies.

The Congressional Budget Office last year estimated that eliminating the tax preferences for investment gains inside permanent-life insurance and annuities would raise an additional $265 billion in taxes over a decade.

Some tax-policy specialists contend the provision artificially favors income in insurance policies over things like interest on bank certificates of deposit. Some also say that because the break enables people who can afford large life policies to accumulate earnings free of taxes, it gives the affluent tax advantages far beyond those available to middle-income people through a 401(k) or IRA.

In 2005, a bipartisan panel appointed by President George W. Bush recommended changes that would have severely crimped tax-free investment gains in life insurance, as part of a broader tax overhaul. The panel said life insurance allows some people to get “nearly unlimited tax-free savings” and that a change would “level the playing field.” The proposal went nowhere.

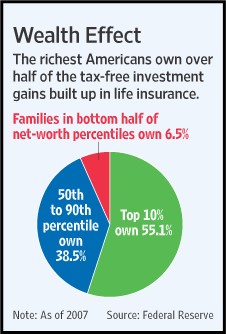

According to Federal Reserve survey data, 22% of assets accumulated tax-free in whole-life and universal-life policies were held by the wealthiest 1% of U.S. families in 2007—those with more than $8.4 million in net worth. More broadly, 55% of the assets in such policies were held by the wealthiest 10% of families. The bottom half by net worth held 6.5% of these assets.

Some of the largest life insurers, seeing the trend, are concerned about a failure to meet what some consider the industry’s social mission to ensure that families have life coverage.

Prudential Financial Inc., which historically has focused on the middle class, says 31% of its new-policy sales in 2009 were to its most affluent slice of customers, households with investable assets over $250,000. That puts them in roughly the top 15% of U.S. households measured by financial holdings, according to Fed figures. A decade earlier, 19% of its policies in force were in that high-end segment.

“If all we do as an insurance industry is focus on the affluent, then I think we can lose sight of the original tenets of life insurance,” said Mark Hug, a Prudential executive.

In an effort to increase sales to middle-income families, Prudential is experimenting with policies for sale through banks that can be issued more speedily. Allstate, MetLife Inc. and ING Groep NV are among other insurers also trying new approaches that aim to sell policies more cost-effectively to the middle class.

Selling to families of modest means was an early focus of the business.

One of the first life insurers, in 1759, was called the Corporation for Relief of Poor and Distressed Widows and Children of Presbyterian Ministers. By the late 1800s, agents from Prudential and other companies were making the rounds in immigrant communities collecting premiums on small policies.

When Congress created an income tax in 1913, it exempted life insurance, in large part because it was seen as providing a safety net.

For decades, whole life, with its tax-free investment component, was the cornerstone of many families’ security. The percentage of families buying such policies began sliding in the 1980s with the proliferation of other savings options such as mutual funds and 401(k) accounts. Some life-insurance agents quit the business, and many who remained moved up-market in search of bigger commissions.

In 1999, an industry-sponsored report discussed agents and companies “migrating toward the upscale markets, leaving the so-called ‘mass market’ behind.”

Trade groups later commissioned a “Task Force for the Future,” which in 2005 said the shift from the middle class toward wealthier customers was eroding the industry’s political clout and undermining the argument for continuing the tax advantages of permanent life insurance.

A study by Conning Research & Consulting in 2006 warned that the industry’s tax benefits could be at risk if “these preferences are perceived to be supporting wealth accumulation or estate planning programs for the wealthy, rather than contributing to protection for widows and orphans.”

An unknown portion of the bulge in sales of large life policies reflects a practice in which older people buy policies and resell them to investors, who pay the premiums and become the beneficiary. Such investor-owned policies don’t enjoy a tax-free death benefit.

This so-called stranger-originated life insurance has faced a crackdown recently and appears to be a dwindling factor.

Many large policies are part of estate planning. In one method, the insured sets up an irrevocable trust to buy a life-insurance policy and pays the premiums by giving sums of money to the trust annually.

This can lower estate taxes, because the trust isn’t considered part of the estate, and the payment of premiums reduces the estate’s size. Then, to the extent estate taxes are due, the insurance proceeds can help cover them.

Steven Oshins, a Las Vegas estate-planning attorney who caters to the wealthy, says he helps arrange about one multimillion-dollar policy a week, policies up to $50 million.

One client is Maryanne Ingemanson, 77 years old, who made a fortune in California real-estate development and now lives on the shores of Lake Tahoe, Nev. A complex plan set up by Mr. Oshins has moved 90% of her net worth into a “dynasty trust” for heirs intended to be passed on tax-free for many generations, she says. A key element is a $20 million policy on the lives of both her and her late husband, which pays out after both are dead.

“It is very satisfying to know that everything you’ve worked for all your life isn’t going to be swept away” in a generation or two by taxes, Ms. Ingemanson said.

A focus on upscale customers was evident at the national conference of the Association for Advanced Life Underwriting, a group of high-end life-insurance agents. “Bullet-proofing Estate Plans Against (Successful) IRS Attacks” was the title of one presentation at the April event in Washington, D.C.

Another expert gave a case study involving a wealthy couple with a family business. He said that, by using a structure combining giant life-insurance policies with trusts and limited partnerships, he cut their estimated future estate-tax bill to less than $9 million, from $46 million.

Michael Kerley, an executive of the National Association of Insurance and Financial Advisors, counts at least 13 “serious proposals” in Congress since 1913 to curb the tax preferences in life insurance. Although legislators have restricted some practices, the core benefits have always survived.

The last serious attempt to tax the investment gains that build up within policies came when the Reagan administration was overhauling taxes in the mid-1980s. Insurers launched a postcard campaign that inundated Congress with mail, and bought TV ads with actors depicting outraged citizens.

“We shouldn’t have to pay a tax for protecting our family,” said an actress playing a young married woman.

- It’s important to remember that the financial strategies of the wealthy often take time to be recognized, understood and assimilated by a CPA before they recommend it to their clients.

- Your securities advisor may have heard about it… but they don’t get a commission for life like they do with “securities” and because of this their Broker Dealer generally won’t allow them to offer it.

To view more articles visit: https://freedomwealthservices.com/news/